说一下Lido的回购

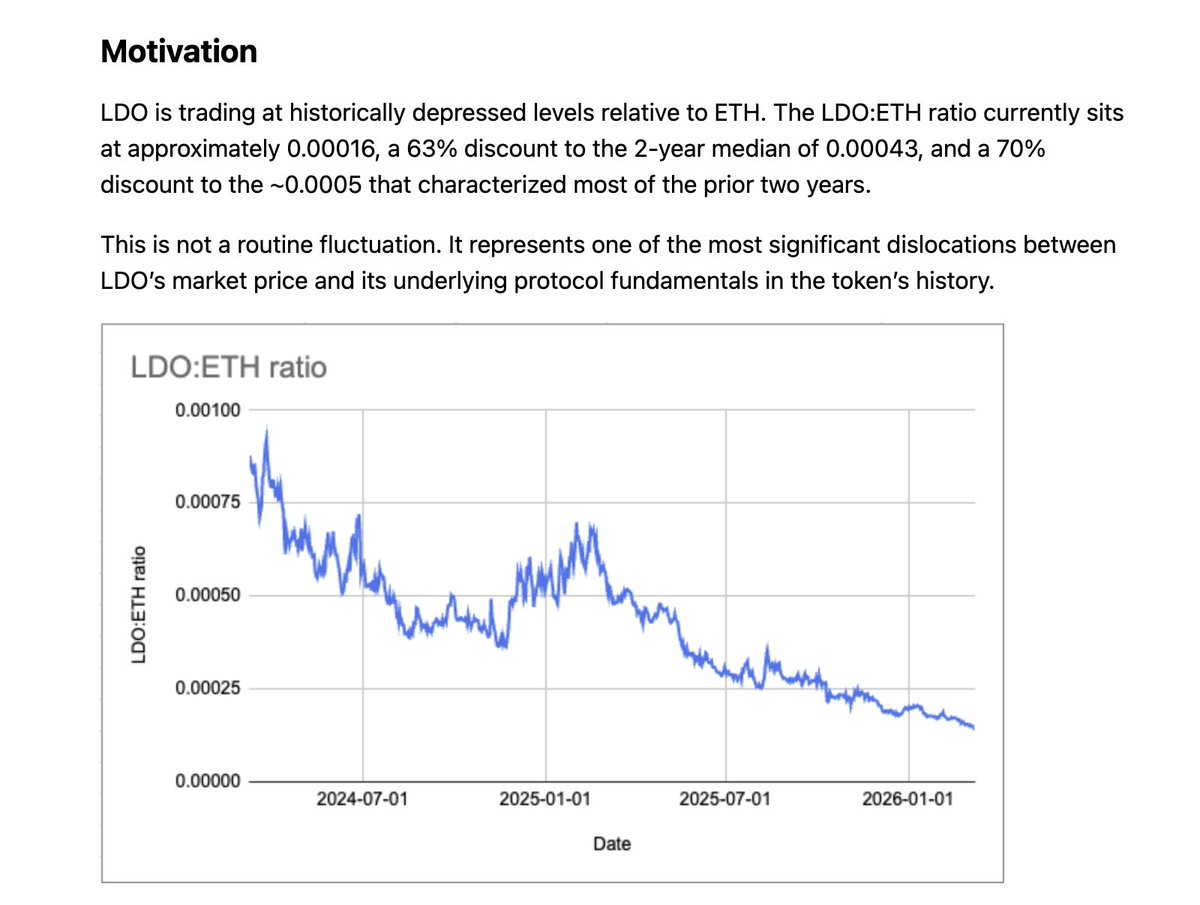

最近Lido发了一个提案,准备了10,000 stETH去回购 $LDO, 动机很简单直接,他们认为LDO对ETH已经超跌了,并给出了一些数据。

当前LDO:ETH大约为0.00016,相比过去两年中位数0.00043低了约63%,而与此同时,协议收入只下降了约 20%。从LDO价格来看,目前基本就是接近历史低点了。

从市值来看也差不多,巅峰期有30亿,目前也就3亿左右了。

比较有趣的是Lido的业务是一如既往的稳定,也简单,一年大概能赚5000-6000万美金左右,但它要分一部分给运营商,那么按照对折来算的话,也有2000-3000万美金。

从这个角度看,挺便宜的,唯一的问题就是staking这个业务是走上坡还是走下坡,老实讲,单纯的staking是一个走下坡的生意,因为这一行的门槛越来越低,同时solo也是逐渐被鼓励的。

那么Lido有没有走上坡的机会,还是有的,就是V3把staking这套服务模块化之后,可以直接对接机构需求,最关键的是能够让其继承stETH的流动性,这一点应该是Lido目前最大的护城河了,如果机构质押有LSD链上流通的需求,Lido是一个不错的选择。

6 years after DeFi Summer, we’re still seeing these massive hacks.

Resolv, Venus Core, and now Drift. For a moment, I thought the Solana VM might be superior on security, with fewer hacks.

Alas. I wonder if low-risk DeFi is a thing. Aave pls hold ground.

All of crypto seems high risk.

我思考了一下,今年到明年,如果要抄底Crypto,标的必须满足:

1/有稀缺性

2/不依赖或者不寄生于外部要素

3/不局限于圈内互卷,有从外面获客或者赚钱的可能性

比如:2018年的 ETH 是有稀缺性的,但是2025年的 ETH 没有稀缺性

市场对OKB的期待是OKX上市,然后OKB拉盘,但事实上OKX上市不会直接对OKB产生影响

新币,绝大部分都是既没有稀缺性,又依赖于外部要素,比如Backpack 之流的Perp 和Opinion之流的预测市场,即没有稀缺性,又依赖于外部要素,大家刷积分不是因为他们本身牛逼,而是Hype和PM 牛逼

Circle,本来是有稀缺性的,但Tether和USD1入局改变了情况

按照这个逻辑,可以选的标的就数的过来了:

1/ $BTC

2/ $BNB : CEX的稀缺性 + 全赛道布局

3/ $HYPE : 链上交易所的稀缺性 + HIP的无限可拓展性

4/ $ZEC :BTC的备份

5/ $MON : 新公链里有技术,并且有最多钱的

还有什么?欢迎补充

Polymarket上的奇葩操作:某初创公司在Polymarket押注自己融资成功,搞懵了投资方。

初创团队在融资轮正式公开10天前,用项目基金会账户(链上标记为“P2P Team”)在 Polymarket 上押注自己能完成 600万美元以上融资。

他们投了约 2.05万美元 的“Yes”份额,当时手里只有 Multicoin Capital 口头承诺的 300万美元,连正式条款书都还没有。

融资最终只募集到 520万美元(没达标),但不过Polymarket 市场价格还是让他们赚了约1.47万美元(提前平仓后拿到3.52万美元)。团队后来把全部利润打进了 MetaDAO 金库。

这几天刷推的一些感想:

1. bp女巫了全世界,edgex明牌老鼠仓被骂后突然拉了个盘,不知是为了爆空头还是以为拉下盘社区就不追责了🤡

好的谢谢 又是被加密暴打的一周 悬着的心终于死了

2. 从上轮牛尾开始 上所=利空 成为共识了,以前将利好全塞在发币前的共识已经彻底烂了。本来crypto有比tradfi有更好的条件去做post-TGE融资比如说协议收入全在链上,资金流实时可查,treasury透明可见,这些优势是tradfi花几十年建审计体系才能勉强做到的事,crypto天然就有。

3. tradfi里IPO后增发 定增 可转债 上市后继续融资是家常便饭,然而crypto没有这种共识,这就是差距,但差距意味着空间,也就是机会。

4. post-TGE融资此前一直有人提但提前一步是天才,提前三步是疯子。因为crypto产品没有真实用户,TGE后就是空城,拿什么去融第二轮?而且每次熊市骂完,牛市新韭菜进场旧模式又能跑一轮。

5. 但这次两件事同时变了:散户不仅被割麻还变聪明了,上所就砸,空投到手就跑,farm几个月分到几十块,这样的学费不需要再交第二次。而且现在信息的透明度和传播速度比以前高太多了,新人进场搜一下就能看到几百条血泪教训。同时crypto第一次有真实经济活动,稳定币在做支付,部分协议在赚真钱,旧叙事没人接了 新的变革有基础了。

6. 下一轮真正的共识升级不一定是全新赛道全新叙事,会是TGE后融资变成正常的事,谁先把这件事做出来,谁就定义下个周期的规则。

前段时间听说 Hyperliquid 背后是 FCoin 的张健。无法确认真实性,也不关心。但从产品和团队角度,这事说得通。

FCoin 2018年推出交易挖矿,上线半个月日交易量号称超币安7倍。Hyperliquid 的 HYPE 空投31%代币零 VC 份额直发用户,价值从18亿美金涨到70亿+,史上最大。两者本质一样:不是撒钱,是设计一个越用越赚、越赚越用的飞轮。

FCoin 核心团队约10人。Hyperliquid 到今天11个人,日均交易量64亿美金,累计2.6万亿接近 Coinbase 两倍,用户从30万涨到140万。11个人。飞轮设计对了不需要大团队。

两者都不拿 VC 的钱。Jeff 用自己量化交易的利润 self-fund,拒绝所有 VC,代币全给社区。FCoin 是最早喊去中心化交易所的,比 DeFi Summer 早两年。张健做过火币 CTO,亲历中心化弊端;Jeff 说 FTX 崩盘是他创业的直接动机。出发点本质一样:见过中心化的脆弱,所以要去中心化。

张健因为 FCoin 一直没现身。FCoin其实不止他一个股东,有多个合伙人,7000到13000个 BTC 的窟窿最后锅全他背了。也能理解这次不会再露面。

这件事让我学到的是:飞轮机制的创新,比 AI、比交易本身都重要。能设计出用户自发传播、自我强化的增长引擎,才是最深的护城河。

这个视频其实还是在讨论一个问题:现在AI行业的空前热闹以及对资金、人才的抽水,会不会“掏空”整个Crypto行业? 答案显而易见,短期会,长期看绝无可能:

1)最近 @VitalikButerin 在a16z播客中表达了对AI权力集中会走向失控的问题。也许现在市场在AI生产力高速飙升期还无感,一旦AI算力、推理、数据等工程能力到达一个瓶颈阶段,围绕去中心化/分布式生产协作关系的需求就会纷至沓来。

我还是那个观点,中本聪当初提出P2P点对点分布式现金系统目标是为了对抗传统金融机构系统的过于中心化,眼下AI突飞猛进也不可避免地走向“中心化”。这种情况下,一种对抗AI中心化的分布式AI Infra也会逐渐被放大需求,这是趋势,不可阻挡;

2)英伟达CEO黄仁勋也在播客中点赞了Bittensor,核心原因就一点,因为 $TAO 的子网用分布式的方式训练了一个72B的Llama类模型,全程没有数据中心、没有白名单、没有超级GPU集群,就靠全球70+个普通贡献者用家用级硬件 + 普通500Mb/s家用宽带,在开放互联网上协作就完成了。

这再一次验证了,AI infra并不都是毫无用处,还是能做出有实用价值的东西的。这又会增进市场对AI +Crypto类基础设施构建的信心。

以上。

不要因短期流动性的抽离而失去信心,AI越成熟越强大,其对底层基础设施的要求就会越苛刻,包括可验证的计算、不可篡改的数据溯源、无需信任第三方的支付结算等等,这些都是Crypto现在主要发力推动的AI Infra主叙事。

至于流动性,迟早会回来的。现在不正是在市场完全不管不顾的背景下为流动性回来构建需求和逻辑的时候?

Saw some people panicking or asking about quantum computing's impact on crypto.

At a high level, all crypto has to do is to upgrade to Quantum-Resistant (Post-Quantum) Algorithms. So, no need to panic. 😂

In practice, there are some execution considerations. It's hard to organize upgrades in a decentralized world. There will likely be many debates on which algorithm(s) to use, resulting in some forks.

And some dead project may not upgrade at all. Might be a good to cleanse out those projects anyway.

New code may introduce other bugs or security issues in the short term.

People who self custody will have to migrate their coins to new wallets.

This brings to the question of Satoshi's bitcoins. If those coins move, then it means he/she is still around, which is interesting to know. If they don't move (in a certain period of time), it might be better to lock (or effectively burn) those addresses so that they don't go to the first hacker who cracks it. There is also the difficulty of identifying all his addresses, and not confuse with some old hodlers. Anyway, it's a different topic for later.

Fundamentally:

It's always easier to encrypt than decrypt.

More computing power is always good.

Crypto will stay, post quantum.

关于BTC的抗量子计算的问题,有人把问题聚焦在算法问题,或者是FUD。

其实,算法从来不是核心问题,技术方案也不是问题,也从来不是FUD的问题,也不是皇帝不急太监急的问题。

问题只有一个:

如何处理暴露公钥地址资金的问题。

是冻结/烧毁?还是谁拿走算谁的?

这里涉及到较大比例BTC的处理:大约25-33%的BTC(大约600-700万枚处于量子暴露状态,包括中本聪的100万,以及其它永久丢失的BTC。

冻结或烧毁会违反BTC社区一直以来的原则:不可干涉,不可篡改。

如果无须冻结这些BTC,谁拿走算谁的。

那么,600-700万枚BTC会被人拿走,假如当时BTC已涨至30万美元一枚,这意味着,这部分总价值在1.8万亿-2.1万亿美元。

这么大规模的BTC流入市场,难以想象,最终的市场会变成什么样子?

现在BTC的量子防护路线,最大的难点,从来不在于技术,而在于治理困境:如何达成社区共识的问题。

其实有个建议:

可以把暴露公钥地址代币纳入到未来的挖矿安全预算。

等未来一天,矿挖完了,这些可以做安全预算的补贴。

同时解决BTC的两座大山:量子计算+安全预算。一举两得。

当然,大概率不会被BTC社区采纳,会遭遇不干预派的激烈反对。

This is wild. Google Research demonstrates a ~20x more efficient implementation of Shor's algorithm that could break ECDSA keys within minutes with ~500K physical qubits.

Google is now are more confident on a 2029 post-quantum transition. We are no longer looking at mid 2030s, we could have quantum computers of this scale by the end of the decade.

They believe this result is so severe that they are not publishing the actual circuits. They instead published a ZKP proving that they know of the quantum circuit with these properties. This is very atypical, showing Google thinks this is serious shit.

All blockchains need a transition plan ASAP. Post-quantum is no longer a drill.

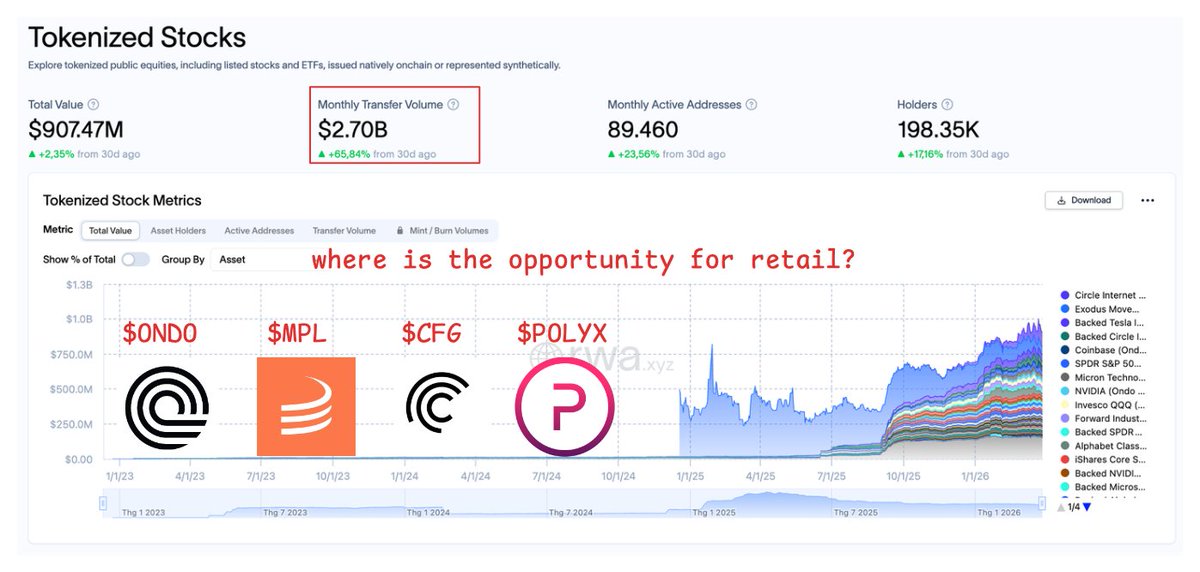

If you ask me what the next market trend is, I would say tokenized stocks 🧵

Because at the end of the day, it’s solving real demand. I personally want exposure to US equities, but there are still too many barriers. Even when access is possible, it often goes through intermediaries, and you still depend on brokers, which adds layers of risk.

That’s why tokenized stocks make sense. It opens access for non-US users to gain exposure to US equities directly onchain.

And it’s quietly becoming one of the biggest narratives within RWA. I believe it’s only a matter of time before this sector accelerates.

If we look at current data:

– Tokenized stocks TVL has crossed ~$1B

– Monthly transfer volume ~$2.5-2.7B

– ~180K–200K holders and ~85K-90K active addresses

– Total RWA market: ~$23-26B (roughly 3-4x YoY growth)

→ The data is already pointing in one direction: this sector is still early and continuing to expand.

What matters even more is capital flow and adoption:

– Ondo holds roughly ~55-65% market share in tokenized securities.

– Franklin Templeton (~$1.5T+ AUM) has launched tokenized funds and is expanding into tokenized ETFs.

– Major exchanges and infra players are actively exploring 24/7 trading rails for tokenized equities.

To understand the upside, zoom out:

The global equities market is around ~$110-115T.

If only 1-5% moves onchain, that’s already a $1T-$5T opportunity.

So where is the opportunity for retail?

In my view, it’s owning the tokens of projects building this infrastructure.

These are the ones I’m watching:

– $ONDO | @OndoFinance leading in tokenized equities and ETFs distribution.

– $MPL | @maplefinance → lending infrastructure for RWA capital.

– $CFG | @centrifuge → tokenization of real-world assets.

– $POLYX | @PolymeshNetwork → compliance-focused chain for regulated securities.

Of course, NFA. DYOR and make decisions based on your own risk profile.

Polymarket said back in December that they wanted to leave Polygon and build their own Ethereum L2.

No chain has shipped yet, no date given, but the intent is out there.

The dependency since then has only gotten worse.

March 2026 numbers:

→ 77% of Polygon's gas consumption

→ 67% of gas fees

→ 55% of all transactions

If you look at the bigger picture, Polygon is highly focused on payments. Stablecoin P2P volume is growing completely independently of Polymarket. That growth is real and it has nothing to do with prediction markets.

But, if you look at the economics, a prediction market generates constant, high-frequency transactions that pay priority fees. A stablecoin transfer costs almost nothing in gas. Those two things are not interchangeable. You'd need dramatically more payment activity to produce the same fee revenue that one prediction market app generates today.

Polygon's team says if Polymarket leaves, blockspace opens up, gas adjusts down, and other apps fill the gap over time.

That's reasonable in theory.

But the claim that Polymarket "isn't most of the chain" by transaction count doesn't hold up, it's 55% of all transactions, not just gas.

The payments story under Polygon is legitimate.

But when a single app accounts for the majority of your chain's activity across gas, fees, and transactions, and that app is openly working on leaving, that's not something you can hand-wave with "other apps will fill the gap."

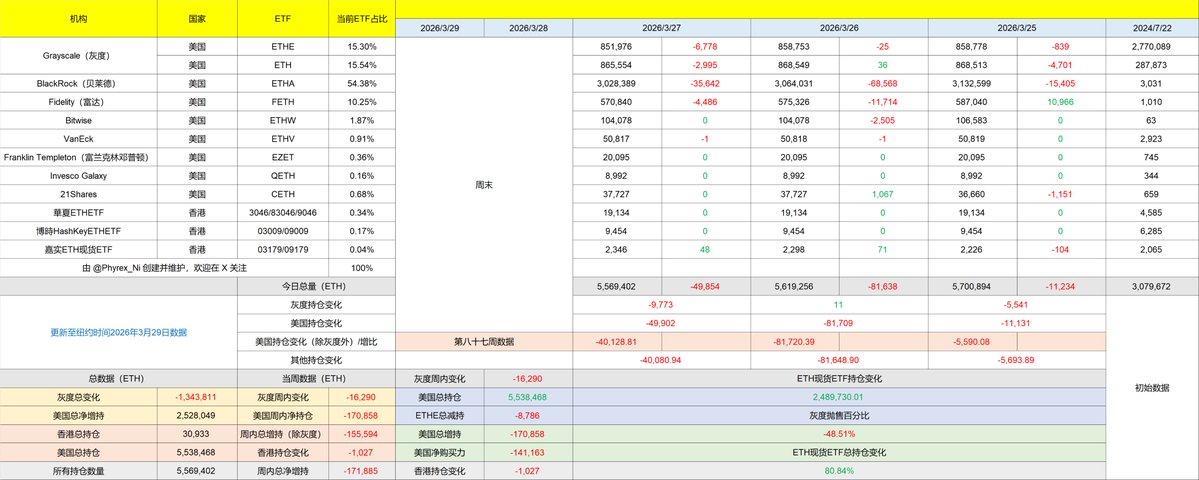

最近 $ETH 的数据都更差了,贝莱德的投资者已经连续两个工作日单日减持都超过 1% 的份额了,过去一周中仅贝莱德一家就抛售了超过 13.8 万枚的 ETH ,超过贝莱德总存量的 4% ,投资者的情绪对于加密货币真的是一塌糊涂,可能 $BTC 还稍微好点,但 ETH 确实难受了。

在刚刚结束的第 87 周的数据中,美国投资者净流出超过了 17 万枚,相比于第 86 周的 7 万余枚,提升了将近 1.5 倍,不过 ETH 确实比 BTC 更早的进入熊市,如果跌破 2,000 美元,加密货币的原生投资者买入还是挺积极的。

#Bitget VIP,费率更低,福利更狠

After a few weeks in SF, one thing stands out: AI people are more bullish on crypto than crypto people are on themselves.

There's this narrative forming in crypto that AI people think crypto is a joke. It's just not true. I keep hearing this over and over from AI people who remain bullish crypto. Hell, Sama, Jensen, Elon, Zuck, the biggest names in AI have all been publicly bullish on crypto and its convergence with AI.

Crypto's problem right now isn't that outsiders don't believe.

It's that insiders are playing scared.

有个问题是,现在的L2会采用吗?

短期看,采用会比较慢,大一些的L2确实不愿意轻易放弃自己利益:

很多L2靠自己的排序器、MEV、gas费、代币经济、桥接费等赚钱。

EEZ要求用ETH作为默认gas、共享流动性、统一框架,可能会稀释他们的“护城河”和收入;

此外,独立L2有自己的治理、升级权、特色功能。加入EEZ框架意味着要遵循共同标准,减少“自定义”空间;此外,目前已有的生态、桥、dApp迁移成本也是有的。

尤其是Base和Arbitrum会先观望,或者部分集成(比如支持EEZ的跨调用,但不完全切换)。

不过,长期看,如果网络效应起来,也有吸引力:

尤其是新项目,一次部署,全EEZ生态(包括主网)都能用,不用重复建流动性、不用维护桥。

用户体验也好,回到“一个以太坊”,不用跳链、记地址。

以太坊基金会支持,Gnosis和Zisk带头,代码全开源(Swiss non-profit形式,目标最小治理、最终不可升级),属于“公共基础设施”。

一些DeFi和RWA协议计划加入。

如果EEZ真做到低gas、高性能、开发者工具好用,网络效应会慢慢拉人进来,就像当年EVM标准让大家统一一样。

当然,也有人质疑,会问:Based Rollup成熟些,问为什么不合作?这样的质疑也是正常。

更多人关心并推进以太坊生态割裂问题,是好事。

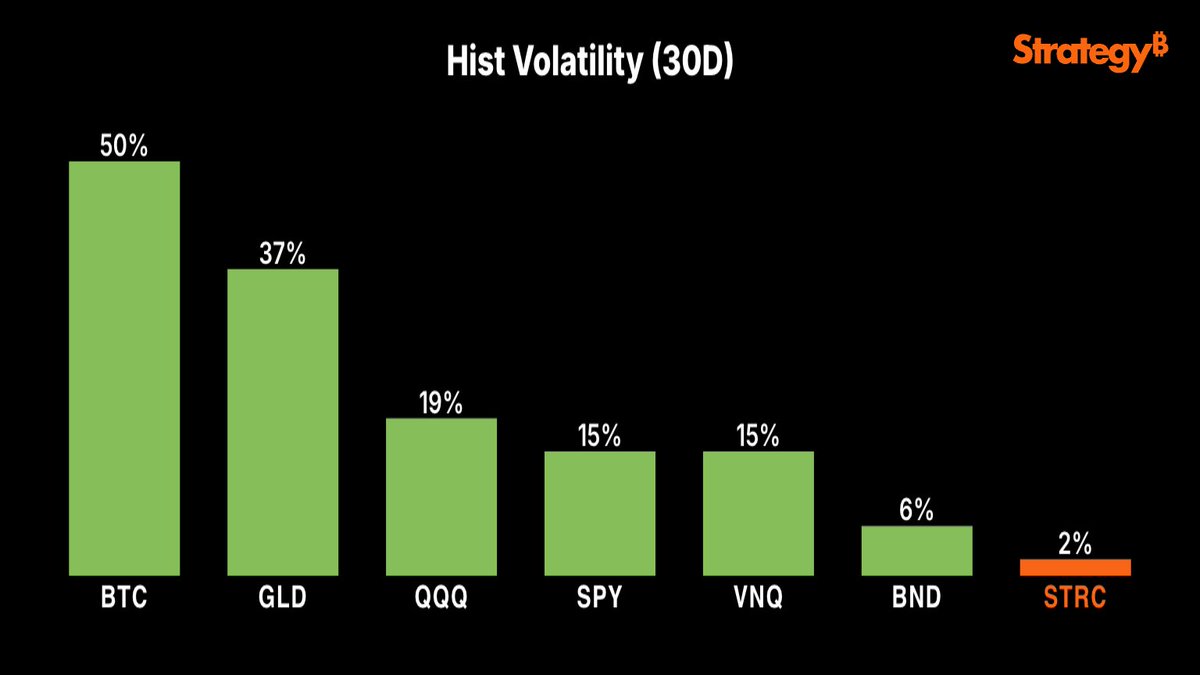

Over the past 30 days, $STRC has been less volatile than every company in the S&P 500—and every major asset class—while delivering an 11.5% dividend yield.

The RWA sector is growing up slowly, but surely. Here's a breakdown of the top assets by active DeFi TVL right now

Data: @DefiLlama https://t.co/ZJvXtcqktr

1) Janus Henderson Anemoy (JAAA) $387.94m

Category: Tokenized Funds

Asset class: Credit / corporate bonds

Access: Permissioned

A traditional asset manager bringing institutional-grade fixed income onchain. The #1 RWA by active TVL.

2) Hastra PRIME (PRIME) - $343.45m

Category: RWA Yield / Wrapped

Asset class: Yield-bearing RWA

Access: Permissionless

One of the few top-tier RWAs anyone can access without KYC gates. A big deal for open DeFi composability.

3) Tether Gold (XAUT) - $140.69m

Category: Tokenized Gold

Asset class: Allocated gold token

Access: Permissionless

Physically backed gold, fully onchain. Permissionless access makes it one of the most accessible hard asset RWAs in DeFi.

3) Superstate USTB - $128.33m

Category: Tokenized Funds

Asset class: Tokenized T-bills

Access: Permissioned

US Treasury exposure wrapped as a token. Superstate placing two products in the top 5 shows strong institutional demand for T-bill yields onchain.

5) Superstate Crypto Carry Fund (USCC) - $121.77m

Category: Tokenized Funds

Asset class: Mixed RWA fund

Access: Permissioned

A hybrid fund blending crypto and real-world yields. Unique in the top 10 - not purely TradFi, not purely DeFi.

6) OnRe Tokenized Reinsurance (ONyc) $110.16m

Category: RWA Lending / Private

Asset class: Reinsurance-backed

Access: Permissionless

Perhaps the most niche asset in the top 10. Tokenized reinsurance risk crossing $110m TVL is a signal of how far RWA innovation has truly come.

7, 8 & 9) ULTRA - $67.06m, Ondo OUSG - $38.59m, US Yield Coin (USYC) - $36.18m

All tokenized T-bill / money market products. All permissioned.

The T-bill trade is clearly dominant as it’s safe, yield-bearing, and familiar to institutions making their first onchain steps.

10/ mF-ONE (MF-ONE) - $25.42m

Category: RWA Lending / Private

Asset class: Private credit pool

Access: Permissionless

Private credit onchain, permissionless. One to watch as private credit tokenization picks up steam in 2025.

Total TVL for RWAS’s is $1.62B, & the top 10 active TVL totals $1.4B, this shows there’s a lack of TVL depth.

7 of 10 are permissioned - institutions are leading

3 of 10 are permissionless but they include gold, reinsurance & yield RWAs

T-bills dominate the asset class mix

Asset diversity is growing: bonds, gold, mixed funds, reinsurance, private credit

目前确实有一些BTC挖矿企业转向AI,不过可以理解,这并不是这一届熊市特有的现象。

目前全球大约15-20%的挖矿产能处于亏损状态(Coinshares数据),运营老旧机器或电价较高的矿企是比较难受的。同时,也有一些矿企为维持运营或者转型,也会把闲置的电力或数据中心转向AI训练/推理,AI租约可以带来更稳定和可预测的收入。

从最近的发展也看到,有些矿企已经签下累计超过700亿美元的AI/HPC合同。这导致有些矿企的AI收入占比要高于挖矿。此外,AI需求暴涨跟矿企现成优势匹配(廉价电力合同/现成数据中心/散热系统和运维经验等)。对于部分矿企来说,这不是逃离BTC,也不单纯是投机,而是生存策略。

历史上类似的事情发生过。2018/19或22年,矿工也曾尝试云服务,其它加密挖矿或能源项目。

几乎每次减半,都会有不少矿工投降,而剩下来的在未来会获得更好的回报。

未离场的矿工往往是更高效的矿工,有更低的电力/新型机器/更低杠杆,当部分算力被出清后,幸存者会得到更多奖励。

也有纯挖矿派,他们没有转向AI,他们的看法是,卖掉算力和BTC去追逐AI,还是短视行为(除非经济压力),长期还是挖矿更香,BTC的安全性和稀缺性最终还是靠ASIC网络维持,而AI是通用算力,竞争更激烈、折旧也更快。

当然,现实很残酷,如果BTC长期在8万美元以下,会给更多矿企带来压力,导致更多产能的关机。

A popular bear case for eth, currently championed by the Canton CEO in this screenshot and trad folks like Austin Campbell, is that institutions will never fully embrace ethereum because they can't or won't suffer the loss of control from permissionlessness.

Dead wrong. This bear thesis makes a fatal mistake in that it ignores how the world actually works.

Regulators, politicians, bank execs, etc. can't look at the world in black and white over a long time horizon, even if the current regulations are black and white.

Every market participant naturally evaluates their alternatives holistically, looking at full spectrum costs and benefits.

Nothing is truly off the table over the long term, even if today's rules or cultures say it's off the table.

Ethereum's permissionlessness has always been theoretically an attractive alternative for banks/institutions because of the two great benefits of a decentralized global hub:

The first benefit of Ethereum is that while you can't subvert permissionless contracts, they can't either. In practice, "they" is a whole lot of parties with conflicting motivations, and now they can trust each other in ethereum agreements by virtue of having removed the trust element.

Humanity has never before had a perfect trust vehicle for digital contracting and exchange. The implications of this are staggering.

The second benefit of Ethereum is access to the world's highest density, freest, and most globalized marketplace.

Institutional participants come for the technology and security/decentralization, but they often stay for the markets.

This is because, as Adam Smith wrote, when you reduce the risk and extend access to a marketplace, the offered goods & services become cheaper, higher quality, and of greater variety. Ethereum is already the best place for many in the world to shop for yield, dollars, euros, gold, certain instruments, etc. This goes 10,000x from here.

We've known for a ~decade that these two benefits of eth (counterparty risk minimization and denser markets) were the theoretical carrot for institutions to voluntarily suffer the stick of reduced control.

How is that theory measuring up as growth progresses?

Well, in the past few years, the theory has begun being proven by empirical reality.

In many jurisdictions around the world, corps, institutions, and governments are actively tumbling down the slippery slope towards permissionlessness on ethereum.

The only way to win to play.

Any country that sits out of Ethereum will cede monetary sovereignty and growth to the countries and institutions that take full advantage of the world's new economic hub and its permissionless distribution.

Ethereum is growing to global ubiquity.

A big part of that will be banks adjusting to the new reality of wanting to opt into permissionlessness - because eth's an amazing opportunity for the early movers and an inevitability for the latecomers.

The fact this is controversial is a big part of why we're still early. ETH

Gnosis虽然看起来在加密领域声量不算太大,但也是多年的老玩家了,也干过不少实事(比如CoW协议、Safe钱包、预测市场框架等)。

Gnosis这里提到说,要帮以太坊构建一个新的L2框架,叫做以太坊经济区, EEZ(Ethereum Economic Zone)。

看到这个提案,还是值得说下。

在过去两年,我们也是一直在唠叨说,阻碍以太坊前进的最大障碍之一,就是L2的分裂,无法跟L1形成合力。

L2的路线,以太坊一开始想法是“扩容”,结果没想到,扩成了数十个孤岛。

开发者也很不爽,一个项目,要在多个L2上重新部署一次、重新接桥、重新找流动性、重新搞钱包……等于把同一个产品复制很多遍。

用户更不爽,钱要跨链桥(又慢又贵),资产散在各个链上,记都记不住,感觉像在很多个不同国家间转账。

也就是说,

以前大家说“以太坊扩容成功了”,其实只解决了“便宜+快”,并没解决“大家还能无缝一起玩”这个根本问题。

EEZ框架的核心就是要解决这个问题。

目标是,让所有EEZ里的L2 + 以太坊主网,像一个链一样实时互动。

技术上叫,“同步可组合性”。

简单说就是:一个交易里就能直接互相调用合约:

不用桥,不用等,不用包装的资产,可以直接用主网的流动性(比如Uniswap主网的池子,你在L2上也能立刻用到);

最重要的是,安全也直接继承以太坊主网验证者(不用自己搞共识)。

这样,

开发者,可以一次部署,整个以太坊L1/L2生态都可以用。

用户,体感上好像回到“一条链”上。

从技术上看,EEZ不是一个具体的链,而是一个新的Rollup框架(类似一套标准模板),让多个L2能跟以太坊L1以及互相之间实时同步组合。

现在普通L2的跨链是“异步”的:你发一个交易过去,要等桥确认、等最终性,可能几分钟到几小时,还可能失败。

EEZ想让它变成“一个交易里就全部搞定”:

合约在L2上直接调用主网合约(或另一个EEZ L2的合约),立刻拿到返回值,继续执行,全程原子性(要么全成功,要么全失败),安全和执行保证跟直接在主网上一样。

从目前披露的情况看,技术上它主要靠实时零知识证明(real-time zero-knowledge proving),由Zisk(Jordi Baylina的项目,他是zk大牛,Circom和Polygon zkEVM核心贡献者)提供证明栈。

简单来说,

• 多个Rollup + 主网的状态通过跨Rollup状态同步机制实时协调(unified state root之类的)。

• 交易执行时,像把几个链“临时当成一个大链”来处理:合约调用跨环境时,ZK证明能快速验证一切正确。

• 不需要额外桥,不需要包装资产,直接用主网的原生ETH作为gas代币,流动性共享(比如主网Uniswap池子,L2上也能直接用到)。

• 安全继承以太坊验证者全套(没有自己的共识机制)。

它不是传统Based Rollup(Based Rollup是L2排序器完全依赖L1排序器/包含,强调去中心化和抗审查)。

EEZ更强调同步可组合性,不是单纯的排序器模式。

它会让EEZ Rollup在L1上结算,并且强调继承L1安全和实时交互,可能在设计上会借鉴或兼容基于L1的机制(基于L1的force inclusion等)。

具体技术白皮书和规格还没发(说是,未来几周会出性能测试、架构细节、开发者工具),现在主要是抽象框架描述。

一句话总结原理:

用实时ZK证明 + 跨Rollup状态同步协议,把多个Rollup和主网“粘”成一个原子执行环境,像一个超级大链一样工作,但每个还是独立的Rollup。

日历

4 月 3 日

数据请求中